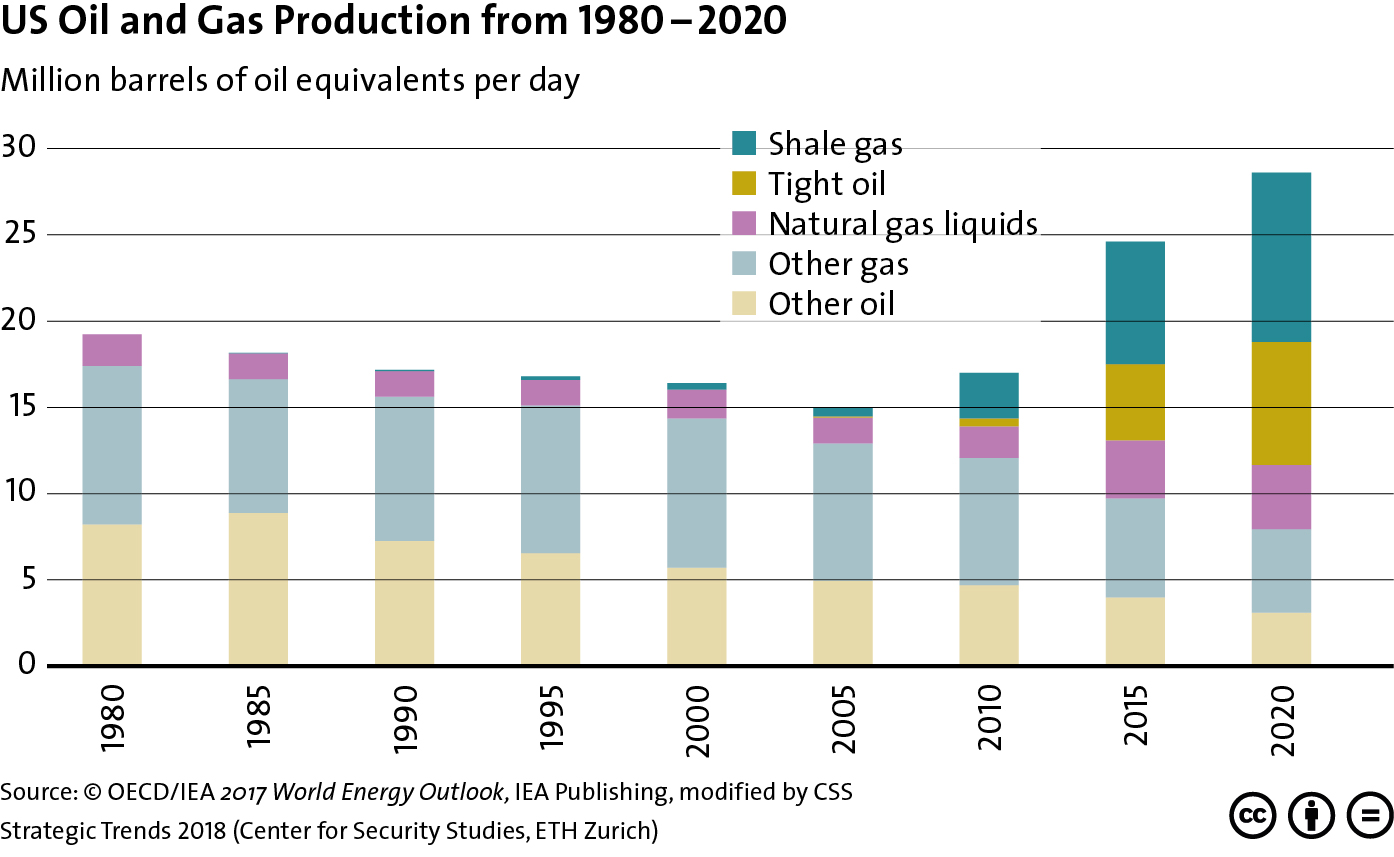

This graphic charts US oil and gas production from 1980 to 2015 and forecasts production up to 2020. For more on the interplay between technological innovation and the geopolitics of energy, see Severin Fischer ‘s chapter for Strategic Trends 2018 here. For more CSS charts, maps and graphics on natural resources, click here.

President Donald J. Trump has strongly criticized the 2015 Paris Agreement on climate reached by President Barack Obama’s administration, arguing that the global deal to cut back carbon emissions would kill jobs and impose onerous regulations on the U.S. economy. As a result, in June 2017 he announced that the United States will exit the agreement. With the United States producing nearly one-fifth of all global emissions, the U.S. withdrawal from the accord could undercut collective efforts to reduce carbon output, transition to renewable energy sources, and lock in future climate measures.

Debate over the impact of withdrawal continues. While Trump has rolled back climate regulations at a federal level, thirty-four states, led by California and New York, have undertaken their own ambitious carbon reduction plans.

What is the status of the Paris Agreement?

The Paris Agreement was finalized at a global climate conference in 2015, and entered into force in November 2016 after enough countries, including China and the United States, ratified it. The nearly two hundred parties to the deal—only Syria and Nicaragua have failed to sign on—committed to voluntary reductions in carbon emissions with the goal of keeping global temperature increases below 3.6 degrees Fahrenheit (2 degrees Celsius), a level that the assembled nations warned could lead to an “urgent and potentially irreversible threat to human societies and the planet.”

President-elect Donald Trump is in the midst of selecting his national security team. He not only needs to decide the “who,” but also the “how” of national security decision-making. It is unclear whether he will adopt Ronald Reagan’s model of entrusting empowered Cabinet secretaries to handle such matters; follow in Richard Nixon’s footsteps of retaining close control over foreign policy within the White House through the National Security Advisor; or emulate George H.W. Bush’s hybrid “gang” blending both White House staff and senior officials.

Beyond his staffing choices, the president-elect and his counselors must also be prepared to tackle a series of questions about U.S. foreign policy and defense strategy, both to inform his continuing selection of personnel to serve in his administration and to shape his conversations with foreign leaders who are anxious to take the temperature of the new Chief Executive. In addition, his answers will be critical if he wants to link his campaign promises with actual policies.

At the 2015 Atlantic Council Energy and Economic Summit in Istanbul, twenty-one Ministers and senior officials from Europe, Asia, North America, and the Middle East met to assess the changing geopolitics of energy security. The assembly was a reminder that energy security — the ability of a nation to secure affordable, reliable, and sustainable supplies to maintain national power — is very different for each nation.

It was clear that advances in technology — in oil and gas, and renewables — have changed the geopolitics of energy dramatically, and mostly for the better, from the world of 2008 or even 2011. We have moved from an era of resource scarcity to abundance, from a concentration of resources to ubiquity of access, and from monopoly power in oil and gas to gas on gas competition in Europe. There is now a clear de-linkage of oil and gas pricing, more hub pricing and a growing spot market in LNG. Floating LNG and containerized shipping are enabling lower cost and quicker access of nations to gas, helping them move away from coal. US shale, with huge resources, low extraction costs, and rapid drilling times may help put a ceiling on the price of oil. Changes in wind, solar, and energy efficiency technology have driven down the cost of renewables in many countries, making them cost competitive with coal or gas in many cases.

Unlike humans some jellyfish are self-sufficient electricity providers. Courtesy of x3nomik/flickr

Europe is talking energy and there is no easy way out of existing dilemmas: While nuclear and fossil-fueled power plants entail considerable risks, most sources of alternative energy are not yet considered mature enough to fuel Europe’s economies on their own. Like elsewhere across the globe, Europeans are facing tough challenges in their attempt to secure a clean, reliable and affordable power supply.

As in every crisis, the risk looms that countries just look after their own narrowly-defined national interests and either ignore or forget the advantages of a regionally coordinated approach. In their struggle for secure energy, European nations should not lose sight of the potential of the common electricity market. In the long run, it could play a crucial role in enabling a more efficient energy future both from an economic and an ecological point of view. Yet, many obstacles still need to be overcome at the moment.

In an integrated market, electricity could be exchanged efficiently across the continent, connecting demand to the most inexpensive supply no matter where in Europe. Consumers could benefit from choosing from a wide range of suppliers, which in turn would boost competition and innovation. Currently, however, the European electricity markets remain regionally fragmented. Countries and companies are not investing enough in transmission capacities across national borders because they struggle to agree on the financial burden-sharing of these expensive projects. As long as national grids are not fully interconnected, trade cannot evolve.